Investing in Opportunity Zones has been gaining increasing attention in the media over the past few months. Congress created qualified opportunity funds (QOFs) as a tool to spur economic development and job creation in certain qualifying low-income communities.

Recently, the IRS published new guidance about the program that we believe made the Opportunity Zone program even more attractive to the right investor. The positive developments include the following:

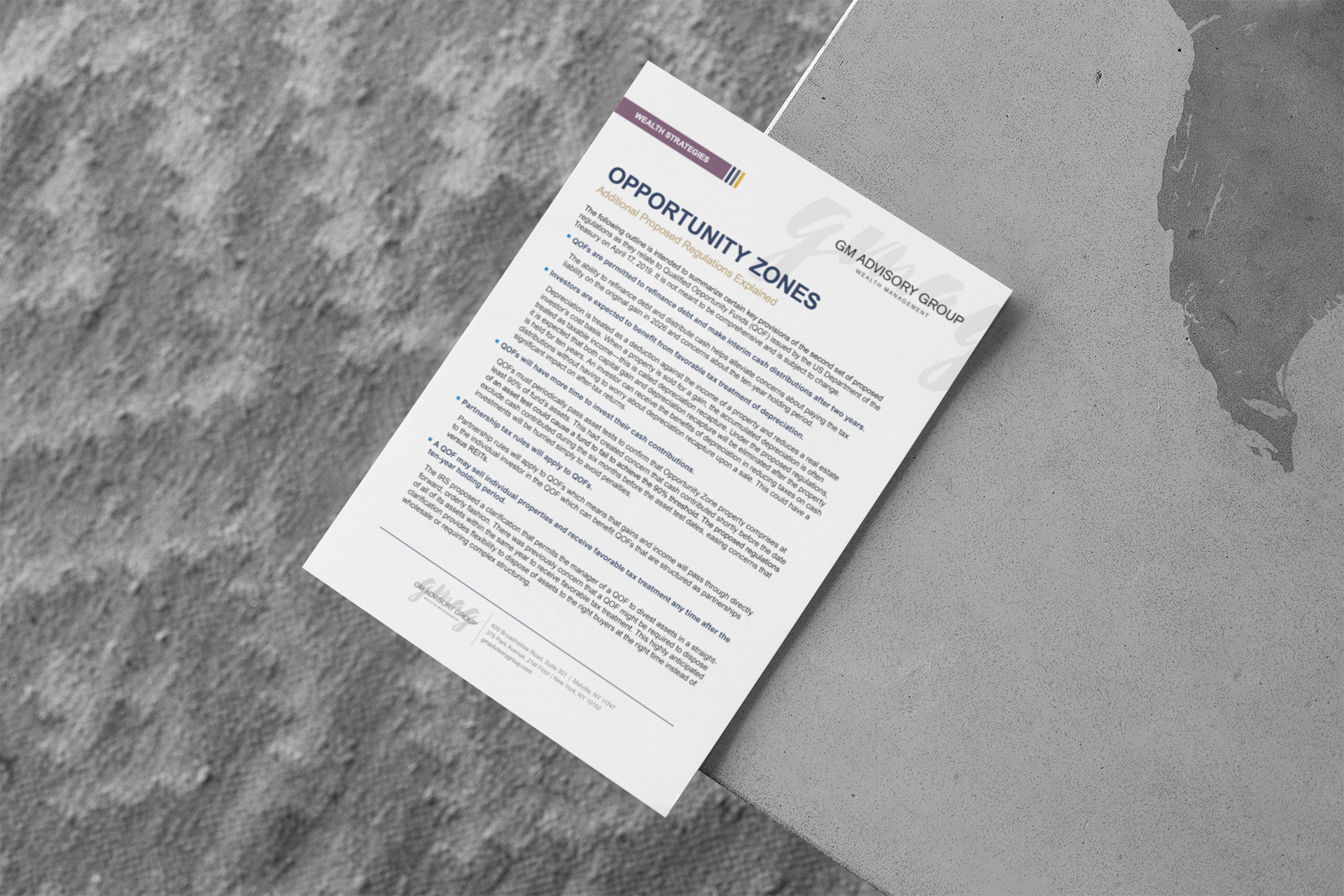

- Improved liquidity

Although investments in QOFs still require a ten-year commitment, the IRS clarified that certain cash distributions are permitted after two years, which could materially improve cash availability during the ten-year investment period. - Improved tax treatment on sale

The IRS proposed eliminating gains on sale that arise from previous depreciation (so-called “depreciation recapture”) and permitting QOFs to sell properties during the ten-year holding period to redeploy capital. - Improved structure

The IRS clarified that the Opportunity Zone program cannot be retroactively canceled, that QOFs will have more time to invest contributed capital, and that partnership tax rules will apply.

Click this link “Opportunity Zones — Additional Proposed Regulations Explained” to review a brief summary memo that elaborates on these and other issues contained in the most recent guidance from the IRS.

Investing in a QOF could be an attractive alternative for investors who have recently realized a capital gain or who are carrying significant unrealized capital gains that they might consider realizing to redeploy that capital to a higher and better use.

If you would like to learn more about the Opportunity Zone program, please click this link to read GMAG’s summary from September 2018. We have plenty of written material on this topic that we would be happy to discuss in more detail. Together we can determine whether this unique investment opportunity might be appropriate for you.